Closing the 90/10 Loophole: A First Look at For-Profit College Reactions

The Higher Education Act’s “90/10 Rule” limits the share of revenue that for-profit institutions can receive from taxpayers through federal education funds to 90 percent of an institution’s total revenue. For decades, the rule’s effectiveness was limited because the federal (i.e., the 90 percent) side was calculated considering only funds from Title IV programs reported by institutions. This created a well-known “loophole” that allowed federal aid flowing to students outside of the Department of Education’s Title IV programs, such as those supporting military servicemembers and veterans (e.g., the GI Bill), to not be counted toward the 90 percent threshold. The result was a strong incentive for for-profit institutions to enroll military students to remain below the limit, while potentially generating up to 100 percent of their revenue from taxpayers.

In 2021, Congress changed the rule to close the loophole. The change requires military and veteran, as well as other non-Title IV, federal educational benefits, to be reported as part of the 90 percent, rather than the 10. This policy brief offers a first look at how the closing of the 90/10 loophole shifted the behavior of for-profit institutions in the year after the change.

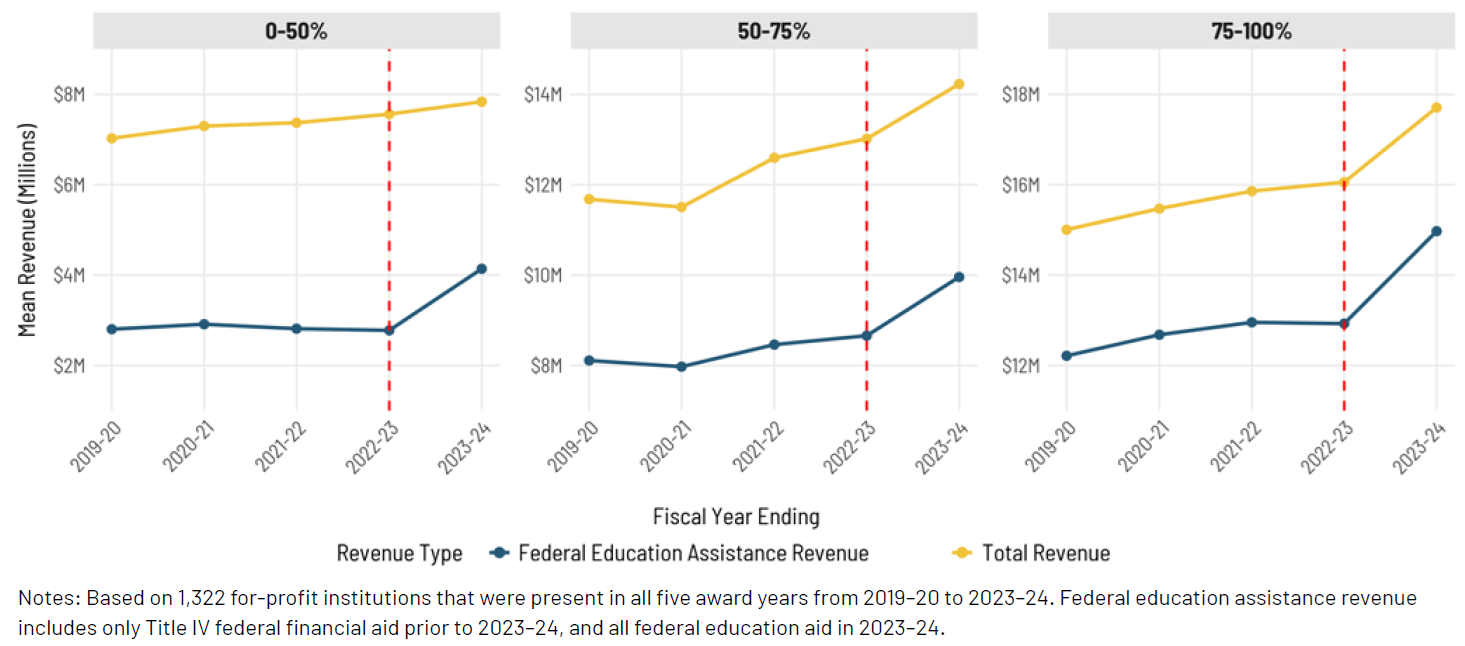

We first document that, as expected, the policy change resulted in an increase in reported federal education assistance funds across the board. As a result, many more institutions were pulled closer to the 90 percent threshold. The number of institutions failing the 90/10 test more than tripled in the first year after the policy change, but failure remains rare: Just 16 schools out of more than 1,400 exceeded the 90 percent limit.

More interesting is that most institutions—particularly those near the threshold in the year prior—found a way to raise their total revenue to offset the increase in the reported federal education funds caused by the rule change. These institutions avoided sanctions and remain in good standing under the revised 90/10 Rule.

We observe that institutions seem to have adopted two different strategic responses to stay below the 90 percent threshold. Some institutions allowed their 90/10 percentage to rise substantially and increased their total revenue only moderately – the new revenue raised was just enough to remain barely under the 90 percent threshold. Others showed unprecedented and sharp increases in total revenue that nearly perfectly offset the effects of the change, leaving their 90/10 percentage unchanged. While more research is needed to understand why and how institutions were able to raise revenue so quickly in response to the closure of the loophole, we find suggestive evidence that institutions may have increased their enrollment of non-Title IV eligible students.

Average Federal Education and Total Revenue Over Time, by 90/10 Levels in 2021–22