The Education Department’s Newest “Professional Degrees” Definition Has a Limited Impact on Financing Gaps

Last year, Congress adopted new federal loan limits for graduate students: up to $20,500 per year for graduate students, and $50,000 per year for “professional” students. The new limits leave a sizable hole in students’ budgets starting this month, with nearly one in three borrowers taking on loans above the new limits, and a likely gap of more than $8 billion annually. A recent court order putting a hold on the regulations that will govern which credentials qualify for the higher caps opens the prospect that some of that hole might be closed, providing liquidity where it was expected to be missing. Using data on the borrowing patterns of past graduate student cohorts, we estimate the amount of new borrowing we might expect as a result of the change – and ultimately find that the change in classification will do little to shrink the hole in student budgets.

The court order stems from a regulatory process that took place over the last year. When the U.S. Department of Education (ED) turned to the finer details of implementing Congress’s vision for loan caps, it hit a roadblock: the statute specified that “professional” degrees needed to meet a definition that already existed in regulation. That definition—which contained a non-exhaustive list of 10 programs such as medicine, law, and even master’s degrees in divinity—provided little clarity about the defining characteristics of a professional degree. The Department established a narrow definition that added only clinical psychology and a handful of adjacent fields to the list of 10, instituted a restriction that professional programs be at the doctoral level, and named several other criteria. The regulation quickly faced litigation from numerous nursing and physician assistant associations.

Just days before the new limits took effect on July 1, a court in that litigation deemed the agency’s definition of “professional” degrees unlikely to survive legal scrutiny, preventing it from moving forward with its list of professional programs. So last Monday night, ED announced a change to implement the court order: an “interim list” of qualifying programs that would be considered professional, at least while the Department continues to fight the case in court. The Department’s barebones announcement included little explanation of its rationale, but changed the list of credentials that qualified for the higher borrowing caps. Now on the list are a number of newly added health fields (nursing and physician assistants, but also physical therapists, occupational therapists, and anesthesiology assistants, among others). Gone from the list are programs that had been included as adjacent to the list of 10 in the existing definition, such as academic theology, certain pharmacy fields, and non-clinical psychology.

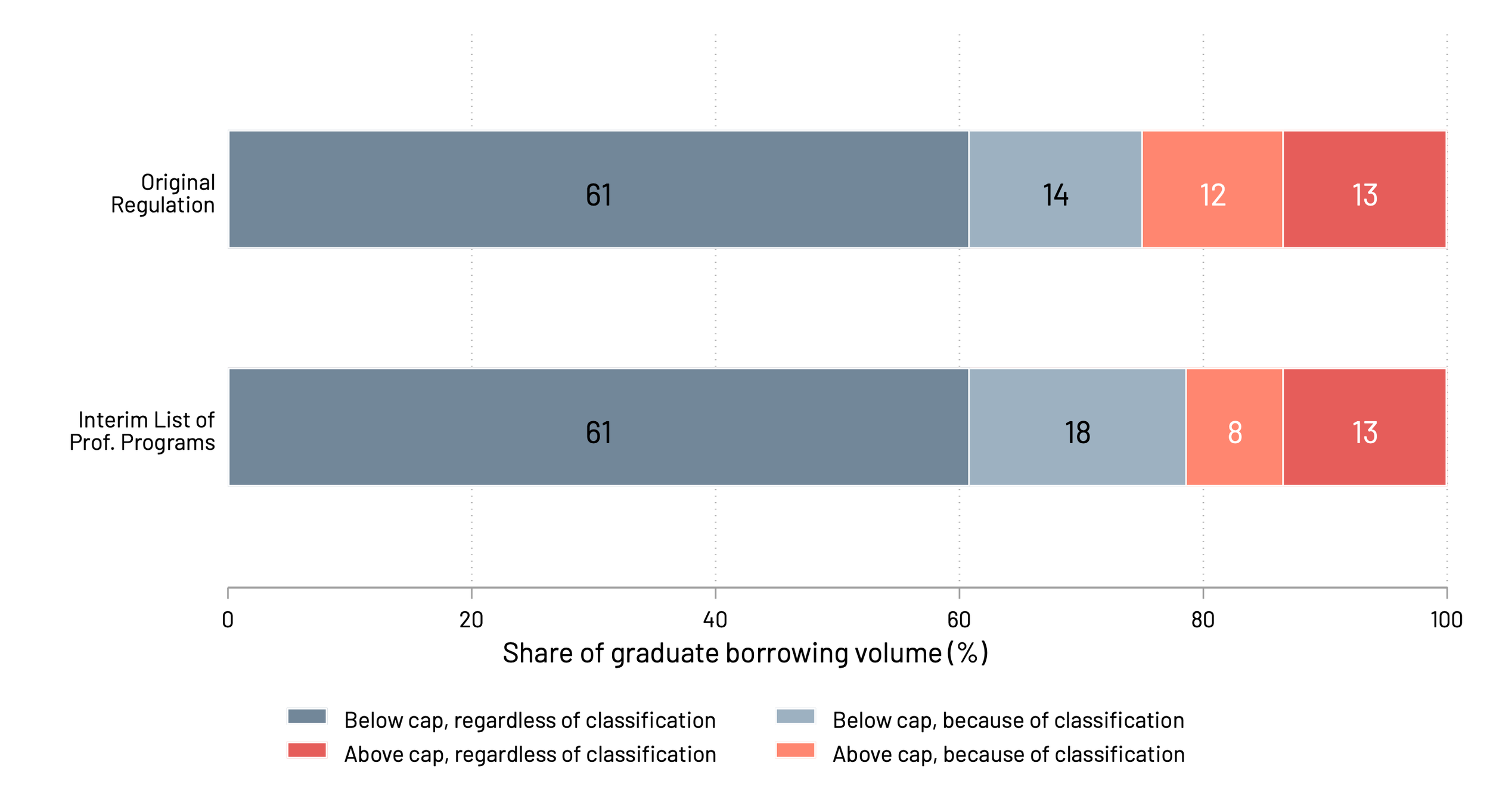

Given how much of the pre-existing demand for federal loans was set to fall out of reach for prospective graduate students, the change to eligible programs raises the question of whether the new rules will meaningfully ameliorate the oncoming borrowing crunch. In Figure 1, we show the overall share of graduate borrowing for past graduate student cohorts (borrowers in award years 2020-2023) above the caps set by Congress, before and after the reclassification. Under the original ED regulation, in the top bar, we estimate that about 25 percent of annual borrowing would be affected by loan caps (the red and peach sections). This includes the 12 percent of loans for graduate degrees that are over $20,500, but below the professional limit of $50,000 (the portion of borrowing that is capped only because of how a program is classified) and the 13 percent above even the $50,000-per-year professional-degree limits (the portion that is capped under any classification).

After the court order this week, the new interim list of professional programs reduced the share of borrowing affected by loan limits slightly, from 25 to 21 percent, as shown in the lower bars in red and peach. As some relatively higher-debt programs were shifted from graduate to professional limits after the court order, the 12 percent of capped volume between the $20,500 and $50,000 limits fell to 8 percent; and the share of borrowing below the caps because of that reclassification (in light grey) grew from 14 to 18 percent.

Figure 1: Graduate Borrowing Above the New Loan Caps, Before and After the Court Stay

Source: ED Office of the Chief Economist, graduate debt data annual borrowing averages for AYs 2020-23. Bar labels report the share of all annual loan volume in the group defined relative to the limit. Dollars above $50,000 in a field facing a $20,500 limit are still placed in the highest group.

These figures suggest the interim list will slightly reduce the overall impact of the new lending caps for some programs. The relative lack of movement in the bite of the caps results from the fact that the limits constrain a great deal of borrowing above $50,000 under any classification framework, where a change in classification would not make such loan-taking allowable. For example, professional areas of study such as medicine and dentistry that already faced a large contraction but will see no relief because they were already allowed to borrow at the highest limits.

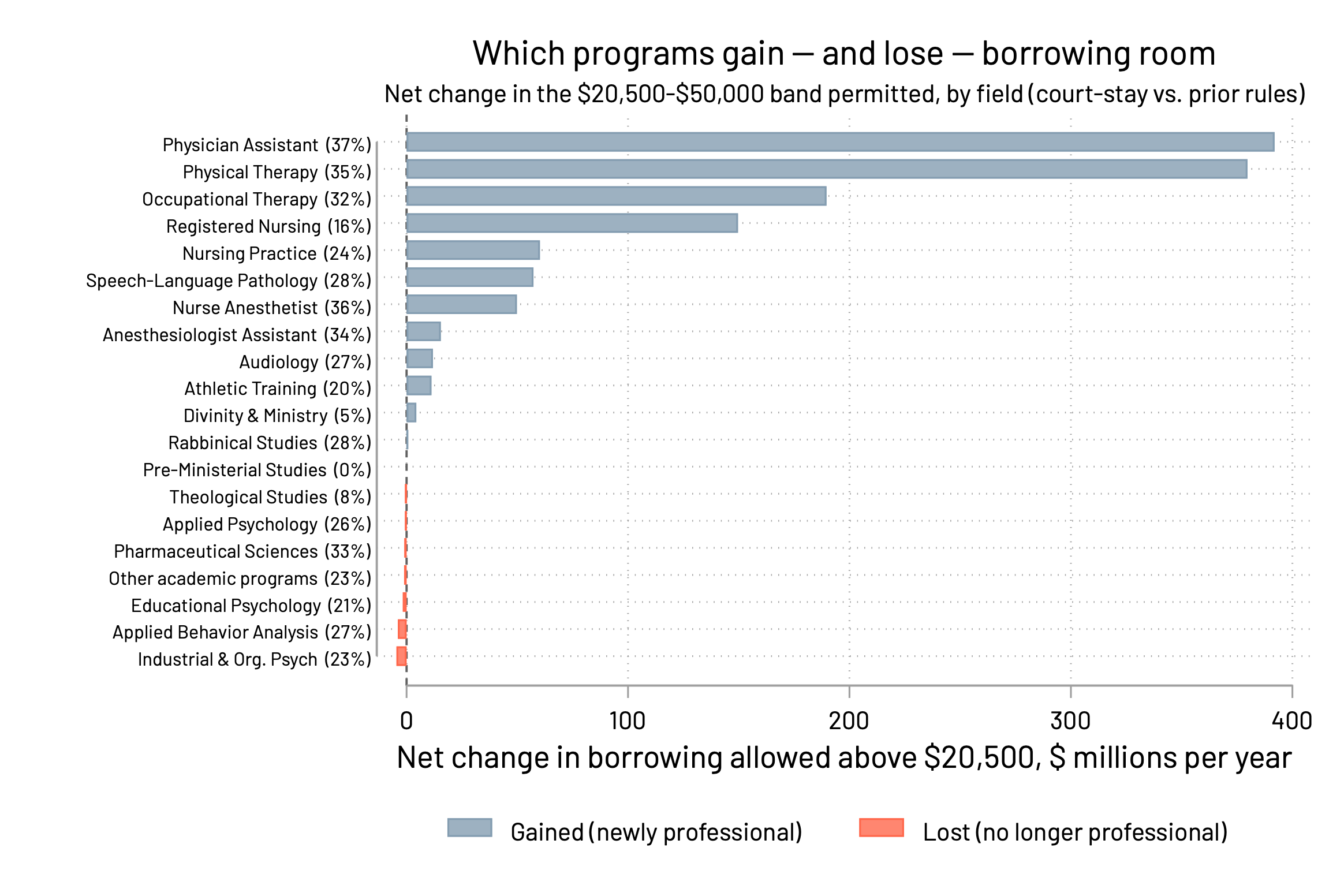

Given this potential for the change to affect fields differently, we explore in Figure 2 how the new interim list of professional programs will ease—or constrain—borrowing limits for each field of study subject to reclassification. Fields noted in blue are those moving from the $20,500-per-year limits to the $50,000; the bars show how much additional lending will be possible under the new, higher limits.

Physician assistants and physical therapists see the greatest amount of increased borrowing room, at more than $350 million in each field per year. The size of that increase accounts for 37 and 35 percent of average annual borrowing in those fields, respectively. Though the occupational therapy field is smaller, nearly $200 million in extra borrowing space per year accounts for nearly one-third (32 percent) of borrowing across the field. Less of the new loan volume will go to other fields, including nursing (about $150 million per year for R.N. programs) and audiology (about $12 million per year). Across all of the newly added fields, borrowers will have access to about an additional $1.3 billion in federal loans annually.

Figure 2: Which Programs Gain–And Lose–Borrowing Room

Source: ED Office of the Chief Economist, graduate debt data annual borrowing averages for AYs 2020-23. Percentages in parentheses reports the change as a share of that field's total borrowing.

The fields with red bars are those being moved off of the professional-degrees list and into the new, lower graduate-level limits. The affected fields are all small (or low-debt) enough that the impact is minor for the overall system, though they may represent a large share of the borrowing in a given field. Across all of these fields, the reduction in annual loan limits means only about $13.5 million in borrowing cuts. Theological studies programs, for instance, see only a small reduction in borrowing room of $574,000, affecting about 8 percent of average annual loan volume across those programs.

For borrowers in the programs that made the interim list of professional programs, this is good news. Among physician assistant programs, for example, we currently find that about 57 percent of loan volume falls above the graduate-level caps; while about 20 percent falls above the new professional-loan caps. Among fields that will be subject to the lower limits, though the overall impact is small, borrowers might feel it acutely within given fields. For instance, pharmaceutical sciences is a very small field and therefore has a small loan volume – but the change means that 37 percent of loan volume, rather than just 4 percent, falls beyond the new, lower caps.

This week's change in which programs count as graduate or professional after the court’s stay has important implications for some reclassified fields. However, overall the change will do little to fill the hole left in student budgets due to graduate student loan limits more generally: Overall affected loan volume will decline only slightly from 25 to 21 percent. Many of the programs most at risk of becoming inaccessible, including medicine and dentistry, remain unaffected.

Still, it appears the process of defining a professional program is far from over. The Department warned in its notice that it will continue fighting for its original definition in court. The stakes remain high for borrowers considering advanced degrees in high-debt fields.

Table 1: Loan Volume and Borrowers Affected by Reclassification of Programs on the Interim “Professional Degrees” List

| Direction of Change in Borrowing Limits | Field of Study (CIP6) | Original regulation | Interim list | ||||

|---|---|---|---|---|---|---|---|

| Volume Affected (%) |

Borrowers Affected (%) |

Volume Affected ($) |

Volume Affected (%) |

Borrowers Affected |

Borrowers Affected (%) |

||

| Expands | Physician Assistant (51.0912) | 57% | 72% | $210.4M/yr | 20% | 9,647 | 41% |

| Physical Therapy (51.2308) | 49% | 63% | $155.2M/yr | 14% | 8,219 | 29% | |

| Occupational Therapy (51.2306) | 44% | 52% | $69.1M/yr | 12% | 3,885 | 21% | |

| Registered Nursing (51.3801) | 21% | 20% | $47.8M/yr | 5% | 2,285 | 4% | |

| Nursing Practice (51.3818) | 32% | 33% | $19.6M/yr | 8% | 1,094 | 11% | |

| Speech-Language Pathology (51.0203) | 37% | 44% | $17.9M/yr | 9% | 1,037 | 15% | |

| Nurse Anesthetist (51.3804) | 57% | 71% | $29.0M/yr | 21% | 1,270 | 42% | |

| Anesthesiologist Assistant (51.0809) | 70% | 92% | $16.9M/yr | 37% | 445 | 66% | |

| Audiology (51.0202) | 34% | 45% | $3.0M/yr | 7% | 203 | 13% | |

| Athletic Training (51.0913) | 23% | 29% | $1.7M/yr | 3% | 145 | 6% | |

| Divinity & Ministry (39.0602) | 5% | 6% | $0.2M/yr | 0% | |||

| Rabbinical Studies (39.0605) | 30% | 47% | $0.0M/yr | 1% | |||

| Contracts | Industrial & Org. Psych (42.2804) | 6% | 9% | $5.8M/yr | 29% | 273 | 31% |

| Applied Behavior Analysis (42.2814) | 5% | 9% | $4.7M/yr | 32% | 249 | 42% | |

| Educational Psychology (42.2806) | 7% | 8% | $2.3M/yr | 28% | 103 | 26% | |

| Pharmaceutical Sciences (51.2010) | 4% | $1.1M/yr | 37% | 68 | 60% | ||

| Applied Psychology (42.2813) | 5% | $0.7M/yr | 31% | 35 | 38% | ||

| Theological Studies (39.0601) | 2% | $0.7M/yr | 9% | 49 | 12% | ||

| Pharmacy & Pharm Sci (other) (51.2099) | 7% | $0.3M/yr | 37% | ||||

| Pharmacoeconomics (51.2007) | 27% | $0.3M/yr | 63% | ||||

| Transpersonal/Spiritual Psych (42.2817) | 17% | $0.3M/yr | 55% | ||||

| Pharmaceutics & Drug Design (51.2003) | 2% | $0.1M/yr | 23% | ||||

| Performance & Sport Psych (42.2815) | 8% | $0.2M/yr | 36% | ||||

| Theological & Ministerial (other) (39.0699) | 4% | $0.2M/yr | 15% | ||||

| Community Psychology (42.2802) | 0% | $0.1M/yr | 12% | ||||

| Pharmaceutical Chemistry (51.2004) | 0% | $0.0M/yr | 7% | ||||

| Pre-Ministerial Studies (39.0604) | 0% | $0.0M/yr | 0% | ||||

Notes: Each row is a CIP6 field whose professional-program status changes between the original regulation and the interim list. "Expanding" fields move from the $20,500 graduate annual cap to the $50,000 professional annual cap; "Contracting" fields move from the $50,000 professional cap to the $20,500 graduate cap. In every column, "affected" means borrowing or borrowers above the applicable annual cap under that regime. Original-regulation columns report the affected share under the PEER prior professional-program definition. Interim-list columns report the affected annual dollar amount, affected volume share, affected annual borrower count, and affected borrower share under the FSA interim list. Dollar and borrower counts are annual averages, calculated by dividing AY2020-2023 totals by four. The $50,000 threshold is linearly interpolated from ED's published $41,000 and $61,500 thresholds. Blank borrower cells reflect suppressed borrower-share inputs; 0% indicates a reported value that rounds to zero.

Source: PEER analysis of ED Office of the Chief Economist GradDebt credential-level by CIP6 aggregates, AY2020-2023, and Federal Student Aid's June 29, 2026 interim list of professional degree programs.